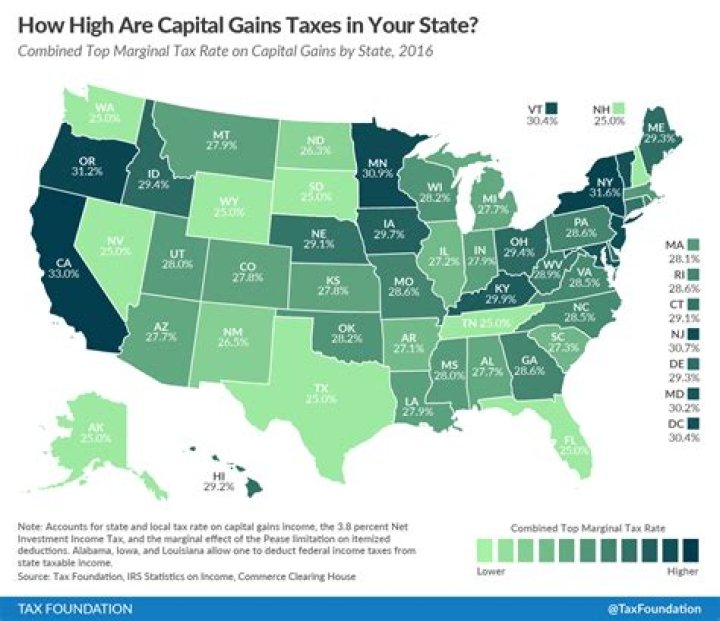

Capital gains are taxable at both the federal and state levels. While the federal government taxes capital gains at a lower rate than regular personal income, states usually tax capital gains at the same rates as regular income. In Idaho, the uppermost capital gains tax rate was 7.4 percent.

How does Idaho tax long-term capital gains?

Idaho’s capital gains deduction Idaho allows a deduction of up to 60% of the capital gain net income from the sale or exchange of qualifying Idaho property. For tax year 2001 only, the deduction was increased to 80% of the qualifying capital gain net income.

Do I have to pay capital gains when I sell my house in Idaho?

If you decide to sell your Idaho house without living in it for two years in this time period, you will have to pay taxes on the capital gains. Selling your Idaho house less than a year after buying it is an even more expensive proposition because then the short-term capital gains tax is going to be applied.

How are capital gains taxed in the state of Idaho?

Capital Gains 1 Forms/publications 2 Qualifying property. Real property. 3 Property that doesn’t qualify. Intangible property. 4 Idaho’s capital gains deduction. Idaho allows a deduction of up to 60% of the capital gain net income from the sale or exchange of qualifying Idaho property. 5 Laws and rules

When do you get a capital loss in Idaho?

A capital loss occurs when you sell or exchange a capital asset for less than the cost or other basis. Idaho allows a capital gains deduction for qualifying property located in Idaho. Gains from the sale of the following Idaho property qualify for the capital gains deduction:

What are the state tax rates for capital gains?

AL, AR, DE, HI, IN, IA, KY, MD, MO, MT, NJ, NM, NY, ND, OR, OH, PA, SC, and WI either allow taxpayer to deduct their federal taxes from state taxable income, have local income taxes, or have special tax treatment of capital gains income.

What are adjustments of foreign capital gains and losses for?

Adjustments of foreign capital gains and losses for the foreign tax credit. The Sec. 901 foreign tax credit available is limited to the amount of tax that would have been paid to the United States on the foreign income giving rise to the foreign tax paid or incurred.