When an S Corporation distributes its income to the shareholders, the distributions are tax-free. Distributions may include amounts that have been taxed in a prior year (as pass-through income), amounts that are taxed in the current year, and/or amounts that have not been taxed at all.

Can an S Corp make distributions?

Distribution from S corporation earnings: Unlike C corporations, S corporations generally do not make dividend distributions. They do make tax-free non-dividend distributions, unless the distribution exceeds the shareholder’s stock basis.

How are S corporation dividend distributions taxed?

S corporations generally make non-dividend distributions, which are tax-free, provided the distribution does not exceed the shareholder’s stock basis. If the distribution exceeds the shareholder’s stock basis, the excess amount is taxable as a long-term capital gain.

Do you pay taxes on profit distribution?

Also, profit distributions are untaxed. Dividends from a regular corporation, by contrast, are taxable income to shareholders — meaning that corporate profits are effectively taxed twice.

How do I pay taxes on a distribution?

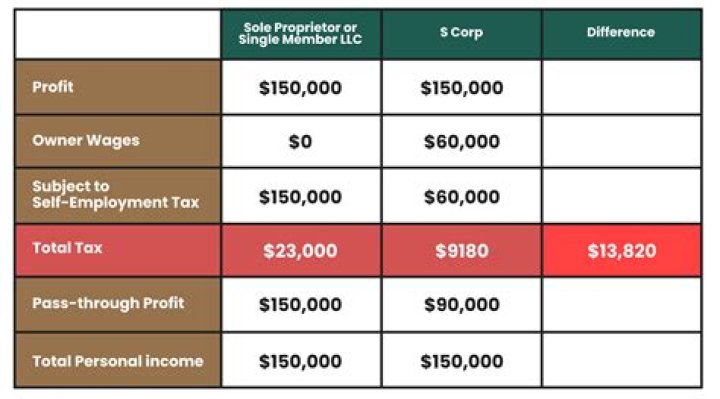

The money you receive as distributed profits works out better for you, when it comes time to pay taxes. If you earn a salary, you have to pay Social Security and Medicare taxes on it. There are no payroll taxes on a distribution of earnings, which has the effect of cutting your taxes substantially.

Where do you report distributions in excess of basis on 1040?

If a distribution exceeds the basis that the taxpayer has in the s-corporation, the difference will be carried to Form 8949, Part II. Box F is checked and the description shows as “Excess Distribution” with the name and EIN of the s-corp listed: Review Wks K1S Detail Adj Basis in view mode for details.

How are shareholder distributions taxed in a S corporation?

S corp shareholder distributions are the earnings by S corporations that are paid out or “passed through” as dividends to shareholders and only taxed at the shareholder level. Unlike a partnership, an S corporation is not subject to personal holding company tax or accumulated earnings tax.

What are the tax consequences of C corporation distributions?

The tax consequences of distributions from C corporation depends on the type of the distribution. Distributions are taxable to the shareholder. Tax Consequences of Distributions from C Corporations Skip to main content Skip to primary sidebar Skip to custom navigation Check out my services page to find out how I can help with your legal issues.

How is a C Corp dividend reported to shareholders?

A regular C corporation distributing its earnings out of retained earnings is considered a dividend. C corp shareholders receive Form 1099-DIV and they will, in turn, report the dividend on their individual federal tax return. S corporations, in general, do not make dividend distributions.

How is income earned by a corporation taxed?

When the income is distributed to its shareholders, it is generally taxed as a dividend. This results in the same income earned by the corporation being taxed twice (double taxation); once at the entity level and again at the shareholder level.