You can only deduct interest on a reverse mortgage when it’s paid. Since most reverse mortgages aren’t paid until the home is sold or the borrower dies, you may never benefit from the tax deduction.

No, reverse mortgage payments aren’t taxable. Reverse mortgage payments are considered loan proceeds and not income. Interest (including original issue discount) accrued on a reverse mortgage isn’t deductible until you actually pay it (usually when you pay off the loan in full).

Is mortgage insurance premium on reverse mortgage deductible?

Deducting The Mortgage Insurance Premium Of A HECM Reverse Mortgage. If ongoing payments to the reverse mortgage are made, the MIP may be deductible (if otherwise eligible), and notably repayments to a reverse mortgage are presumed to be allocated towards the (accrued upfront and ongoing) MIP first.

When to claim interest on a reverse mortgage?

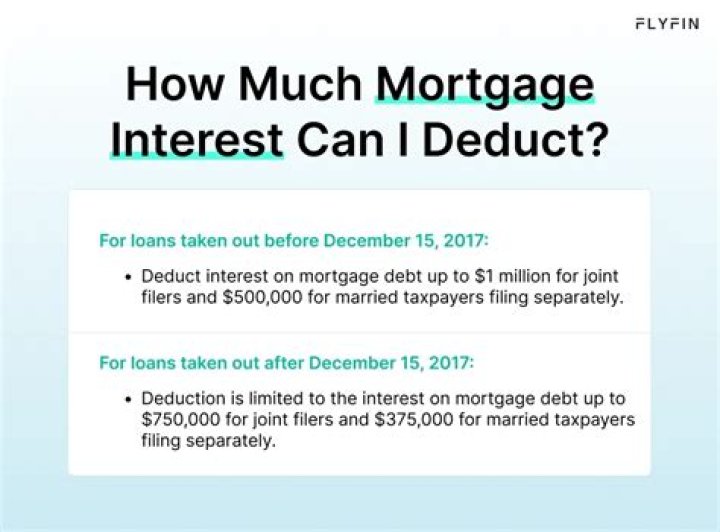

If you move or sell the home, however, the loan becomes due along with accumulated interest payments. The IRS considers reverse mortgages to be a form of home equity loan. As with a traditional mortgage, interest on a reverse mortgage is deductible; however, this deduction is limited to interest paid on no more than $100,000…

What kind of payment does a reverse mortgage make?

Reverse mortgage payments are considered loan proceeds and not income. The lender pays you, the borrower, loan proceeds (in a lump sum, a monthly advance, a line of credit, or a combination of all three) while you continue to live in your home.

Can you deduct broker fees on a reverse mortgage?

Although you can’t deduct interest on a reverse mortgage until you actually pay it, you can deduct the fees and costs of originating the loan. These include broker fees, document fees and “points” charged to you in return for a lower-than-market interest rate.

When does principal increase on a reverse mortgage?

After the first month of your HECM loan, the principal limit increases each month thereafter at a rate equal to one-twelfth of the mortgage interest rate in effect at that time, plus one-twelfth of monthly mortgage insurance premium rate. This growth should be considered a further extension of credit rather than an accrual of interest.