Social Security income for retirement or long-term disability can typically be used to help qualify for a mortgage loan. That means you can likely buy a house or refinance based on Social Security income, as long as you’re currently receiving it.

Do you need your Social Security card to refinance?

Social Security Number: The social security number is needed for anyone who is on the mortgage loan. This information can be verified through a social security card, any tax documents, or other documents that show your social security number. Your SSN is used to verify your identity and to pull up your credit.

Do mortgage lenders need your Social Security number?

Lenders need your Social Security number to run a credit check so they can see your credit score. Once they see your credit scores, they match this information with the Social Security number you provide to verify all the information is correct.

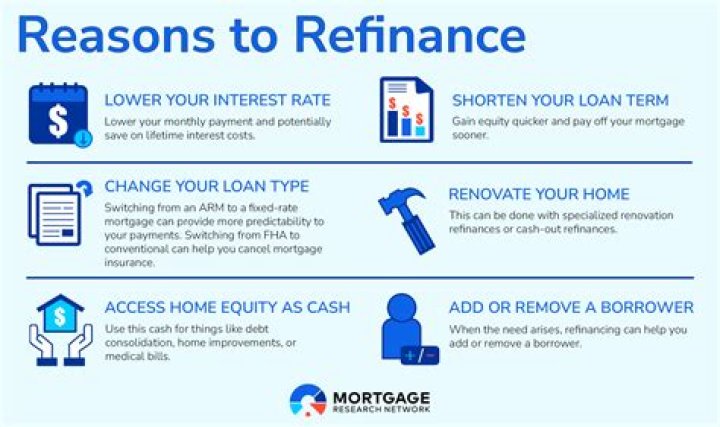

What do you need to know before refinancing your mortgage?

9 Things to Know Before You Refinance Your Mortgage. 1 1. Know Your Home’s Equity. The first qualification you will need to refinance is the equity in your home. At the end of the first quarter of 2020, 2 2. Know Your Credit Score. 3 3. Know Your Debt-to-Income Ratio. 4 4. The Costs of Refinancing. 5 5. Rates vs. the Term.

How much equity do I need to refinance my home?

Home equity: Check your home equity balance. To save on PMI, the amount of your refinance loan will need to be less than 80% of the value of your home. Home condition: Lenders may require an appraisal to assess your home’s value, which helps them determine how much money they’re willing to loan you.

What should my credit score be to refinance my home?

Borrowers with credit scores of 620 or greater may be eligible to refinance their home, but credit scores of 740 or higher receive the most favorable refinance interest rates. The higher your credit score the lower your refinance interest rate, so it’s beneficial to have a healthy credit score.