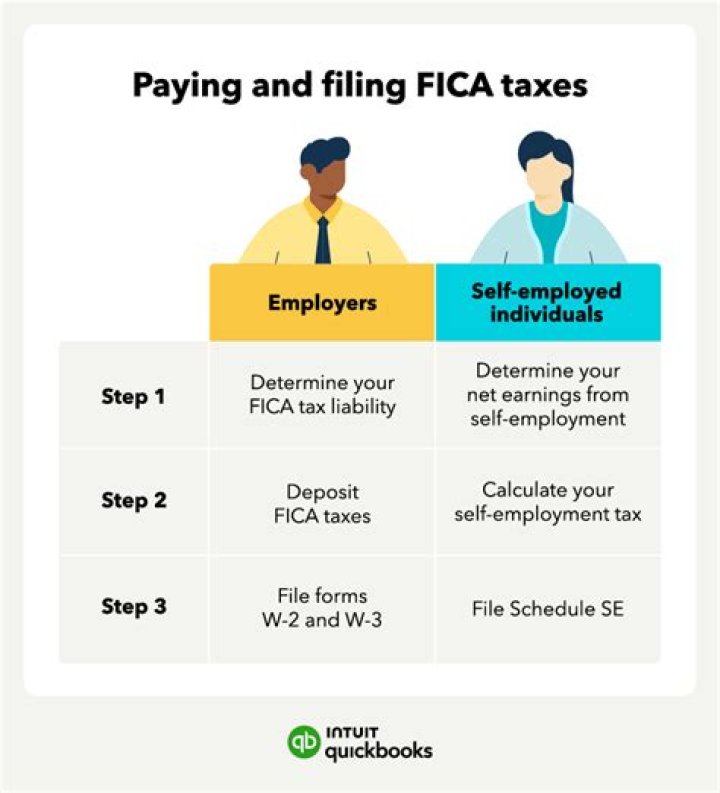

FICA (Federal Insurance Contributions Act) taxes are social security and Medicare taxes that both employers and employees pay. Employers must withhold FICA taxes from employees’ wages, pay employer FICA taxes and report both the employee and employer shares to the IRS.

Who is exempt from FICA and Medicare?

Thus, to summarize, both the Internal Revenue Code and the Social Security Act allow an exemption from Social Security/Medicare taxes to alien students, scholars, teachers, researchers, trainees, physicians, au pairs, summer camp workers, and other nonimmigrants who have entered the United States on F-1, J-1, M-1, Q-1.

What happens if employer does not pay employee portion of FICA?

If such a deduction from the employee’s remuneration to pay the employee portion of the FICA tax on the wage is not made, the obligation of the employee to the employer with respect to the undercollection of the employee portion of the FICA is a matter for settlement between the employer and the employee.

Can a private company deduct fica from your paycheck?

The rules do not apply only to private companies – the case cited by the CA labor relations board was where the State of CA overpaid public employees and tried to deduct the overpayment from their paychecks without their permission – the court said the state could not do that.

Is there an employer match for Medicare Futa?

There is no employer match for the Additional Medicare Tax. For additional information see our questions and answers. Employers report and pay FUTA tax separately from Federal Income tax, and social security and Medicare taxes. You pay FUTA tax only from your own funds. Employees do not pay this tax or have it withheld from their pay.

Is the 6.2% tax not withheld for FICA?

The information posted on PayrollTalk is for informational purposes only and is not intended to substitute for obtaining accounting, payroll, tax, or financial advice from a professional accountant. An an employer did not withhold the 6.2% for FICA for 3 years for an employee.