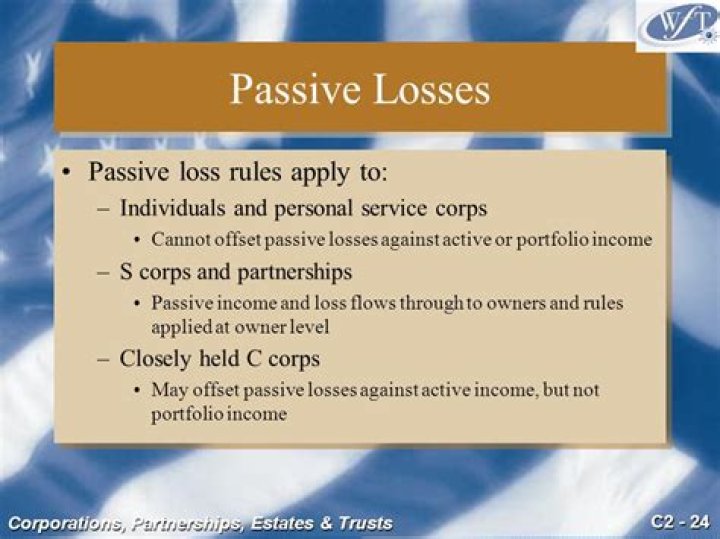

Passive activities are trades, businesses or income-producing activities in which you don’t “materially participate.” The passive activity loss rules also apply to any items passed through to you by partnerships in which you’re a partner, or by S corporations in which you’re a shareholder.

Are S Corp distributions considered passive income?

If you have Schedule K-1 income that is generated from an S corporation, and you were actively participating in the business, then it would be non-passive. It is not automatically earned income or passive income.

Can a taxpayer use a suspended loss on passive activity?

Losses (and credits) that a taxpayer cannot use because of the passive loss limitation rules are suspended and carry over indefinitely to be offset against future passive activity income (Sec. 469 (b)). A taxpayer can apply suspended losses against passive activity income from any source, not just from the activity that created the loss.

Can a C corporation offset losses against passive income?

Under the regulations, the losses continue to be passive and can only be offset against passive income if the C corporation continues to conduct the same passive activities (Regs. Sec. 1. 469 – 1 (f) (4)). The regulations do not say what happens if the C corporation disposes of the passive activity that gave rise to the passive income.

How are passive losses carried over to the next year?

Passive losses and credits are carried over to the next year but may only offset passive income or tax attributable to passive activities.

What happens if C corporation disposes of passive activity?

The regulations do not say what happens if the C corporation disposes of the passive activity that gave rise to the passive income. However, it seems logical that the suspended losses would be deductible against nonpassive income at that time, as if the S corporation disposed of the activity.