Some examples of accrued liabilities include the following:

- Services and purchases that have been received, but the vendors’ invoices have not yet been recorded in Accounts Payable.

- Accrued employee wages and fringe benefits.

- Accrued management bonuses.

- Accrued interest on loans payable.

- Accrued advertising and promotion.

An accrued liability represents an expense a business has incurred during a specific period but has yet to be billed for. There are two types of accrued liabilities: routine/recurring and infrequent/non-routine. Examples of accrued liabilities include accrued interest expense, accrued wages, and accrued services.

What do we mean by accrued liabilities?

Accrued liabilities explained Accrued liabilities, also referred to as accrued expenses, are expenses that businesses have incurred, but haven’t yet been billed for. These expenses are listed on the balance sheet as a current liability, until they’re reversed and eliminated from the balance sheet entirely.

Is an accrued liability a payable?

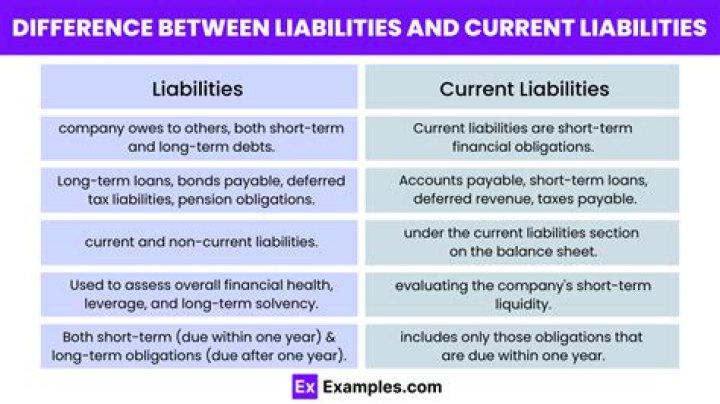

Accrued Liability vs. But there is a difference between the two. While accrued liabilities are for goods and services whose payment is due in the future, accounts payable represent expenses that are due immediately or within the same year as they are incurred.

How do you calculate accrued liability?

Accrued Liabilities

- It exists only in an accrual method of accounting.

- Accrued liabilities usually are periodic and are paid in arrears, i.e., after consumption.

- In the next accounting period, when payment is made, you need to reverse the original entry.

- As per the Accounting Equation, Assets = Liabilities + Equity.

What is the difference between accounts payable and accrued liabilities?

Accrued expenses are those liabilities that have built up over time and are due to be paid. Accounts payable, on the other hand, are current liabilities that will be paid in the near future.