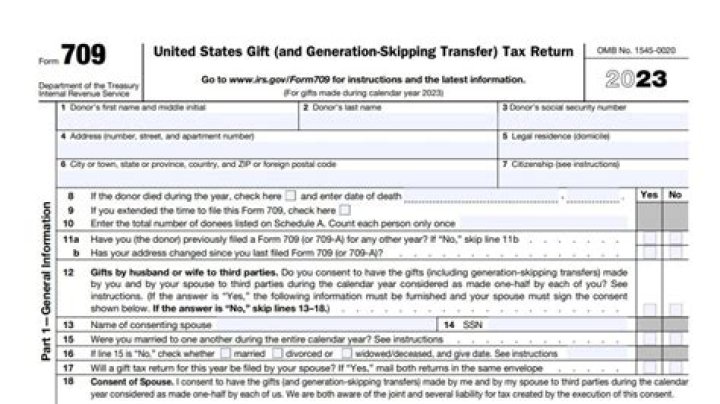

IRS Form 709 reports transfers of assets that may be subject to federal gift tax and certain generation-skipping transfer taxes. This form reports taxable gifts you make to others during your lifetime, including gifts of cash or tangible physical assets, such as real estate.

How does the lifetime gift tax exclusion work?

The annual federal gift tax exclusion allows you to give away up to $15,000 in 2020 to as many people as you wish without those gifts counting against your $11.58 million lifetime exemption. (After 2020, the $15,000 exclusion may be increased for inflation.)

Use Form 709 to report: Transfers subject to the federal gift and certain generation-skipping transfer (GST) taxes. Allocation of the lifetime GST exemption to property transferred during the transferor’s lifetime.

When do you need to file a Tax Form 709?

Certain types of financial gifts may qualify as exclusions for the gift tax. Generation-skipping tax ensures that the proper amount of estate tax is paid when a generation-skipping trust transfers assets among family members. Form 709 must be filed each year you make a taxable gift and included with your regular tax return.

Where do I find the unified credit on Form 709?

It is located on the first page of Form 709. Refer to the “Table for Computing Gift Tax” under instructions to calculate the tax on the amount of reported gift or gifts. You may apply your lifetime gift and estate tax exemption, also known as the unified credit. So you don’t have to pay an out-of-pocket tax if you use this exemption.

When to use Form 709 for generation skipping?

This form reports taxable gifts you make to others during your lifetime, including gifts of cash or tangible physical assets, such as real estate. It’s also used to allocate lifetime generation-skipping tax exemptions when transferring property to a beneficiary (other than a spouse) who is at least 37½ years younger than the donor.

Do you have to pay taxes on a 709 gift?

Before you start creating a 709 form sample, you need to check if you have to. Note that not each transfer requires payment of taxes. Here you will find the list of cases when a blank is needed: you gave gifts to someone totaling more than $14,000 (other than to your spouse); you made transfers called future interests;