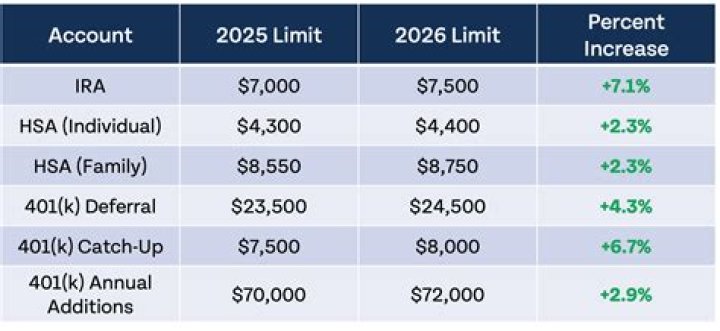

Contributions an employer can make to an employee’s SEP-IRA cannot exceed the lesser of: 25% of the employee’s compensation, or. $57,000 for 2020 and $58,000 for 2021 ($56,000 for 2019)

Can you make a SEP IRA contribution after April 15?

For 2020 only, the April 15th deadline was moved to May 17, 2021. As a result, it is possible for a sole proprietor who has extended their personal return to make 2020 SEP IRA contributions up until October 15, 2021.

What is the deadline to contribute to a SEP IRA?

2020/2021 – SEP IRA Contribution Limits The maximum amount that can be contributed to a simplified pension plan (SEP) is 25% of an employee’s compensation, which is capped at a maximum as indicated above. 2020 SEP IRA Contribution Deadline is 4/15/2021. 2021 SEP IRA Contribution Deadline is 4/15/2022.

When is the deadline to contribute to a SEP IRA?

The contribution deadline is usually April 15 or the tax deadline of the following year — i.e., you have up to April 15, to contribute for the past year’s SEP IRA. The table below shows the SEP contribution limits over the last few years along with some other key figures Can catch-up contributions be made to a SEP?

How are SEP IRA contributions different from other IRA contributions?

SEP IRA contributions are a little different than other IRA contributions. In short, SEP contributions are designated as a contribution for the calendar year in which they are made. From the IRS website:

Why is last year contribution shown on SEP IRA Form 5498?

From the IRS website: Why is last year’s contribution that was made this year for the SEP-IRA shown on this year’s Form 5498 instead of last year’s Form 5498? The IRS requires contributions to a SEP-IRA to be reported on the Form 5498 for the year they are actually deposited to the account, regardless of the year for which they are made.

How much can you withdraw from a SEP IRA?

The result is then multiplied by 20% to arrive at the maximum SEP deduction, $9,293. SEP contributions and earnings are held in SEP-IRAs and can be withdrawn at any time, subject to the general limitations imposed on Traditional IRA. A withdrawal is taxable in the year received.